Accounting is the most critical aspect of the financial activities. A proper accounting system ensures the smooth functioning of the organization. Accounting activities are subject to the accounting standards mentioned by accounting authorities or government bodies.

Similarly, in India, Income chargeable under the head “Profits and gains of business or profession” or “Income from other sources” shall, subject to the provisions of income computation and disclosure standards(ICDS). ICDS are notified by government of India in the official gazette from time to time.

ICDS:

ICDS are applicable to all types of persons earning Income chargeable under the head “Profits and gains of business or profession” or “Income from other sources”. The provisions of ICDS will also be applicable to the persons computing income under the relevant presumptive taxation scheme. In a general scenario, ICDS are applicable to all types of taxpayers who are liable to tax audit. Applicability of Tax Audit is irrespective of the turnover or income limit.

Few Important points related to ICDS:

ICDS being income computation and disclosure standards are closely linked to accounting standards. It follows the footprints of general accounting standards to monitor the disclosure requirements in Income Tax. Audit reports have disclosure requirements of ICDS. Some of the important points in relation to ICDS are mentioned below:

- If there are any conflicts in terms of dealing with an issue in income tax, then the income tax act will always prevail over the ICDS.

- It will not have any impact on MAT calculations for computation of income for companies.

- ICDS are principles laid down for computing income.

- CBDT has clarified that the books of account are to be maintained in accordance with the accounting policies applicable to the assessee.

- An Individual or HUF, who is not required to get his books of account audited for the previous year under section 44AB, shall not be required to comply with the requirements of ICDS.

- ICDS disclosure is to be made in clause 13 of 3CD Audit report.

- ICDS are required only if Mercantile system of accounting is followed.

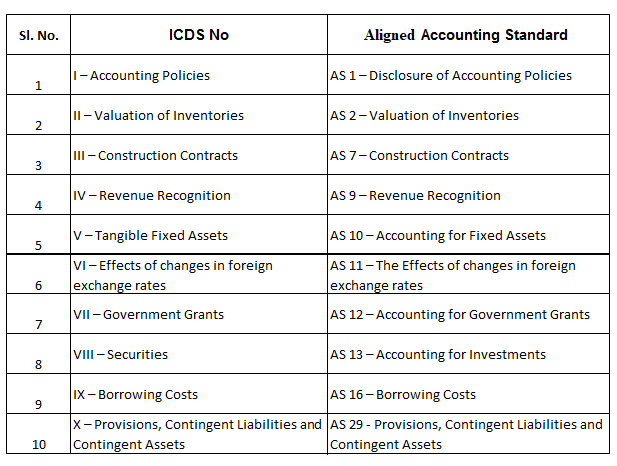

List of ICDS as notified by Income Tax:

ICDS I – Accounting Policies

ICDS II – Valuation of Inventories

ICDS III – Construction Contracts

ICDS IV – Revenue Recognition

ICDS V – Tangible Fixed Assets

ICDS VI – The Effects of changes in Foreign Exchange Rates

ICDS VII – Government Grants

ICDS VIII – Securities

ICDS IX – Borrowing Costs

ICDS X – Provisions, Contingent Liabilities and Contingent Assets

Let us have a look at the ICDS aligned with Accounting Standards:

Conclusion:

ICDS are the computation and disclosures standards notified by government as guiding principles for computing income to align the computation in income tax and accounting. There are no illustrations or examples given in ICDS. Important aspects of ICDS in income tax is the reporting of them in the 3CD audit reports. Since, ICDS are linked to the accounting standards, general principles of Accounting Standards also apply to the ICDS. However, Income Tax Act will always prevail over the accounting standards when it comes to computing of income for taxation purposes.

About Author:

CA Chinmay Shirish Agate

Chinmay Agate is a Practicing Chartered Accountant having 4+ years of experience and expertise in the field of Direct Taxation and Auditing compliances. In the past, he worked in various CA firms and comes with wide industry experience from services, retail to manufacturing to trading where he has handled various complex assignments. He has keen interest in Forex and Derivative knowledge as well as fundamental analysis.

Recent Comments