Stock market is a place where various stakeholders of the society invest their corpus with a purpose of generating wealth. Companies willing to raise funds make an offer to public and other players of the industry. This process of making offer to public for asking their investments and issuing shares to them is called initial public offering i.e. IPO. In current scenario, many IPOs are performing good and investors can enjoy a good premium when such shares are listed. We will discuss the tax implications on such listing gains.

Capital Gains:

Tax on transfer of capital assets is based on the period of holding i.e. whether a capital asset is short term capital asset or a long term capital asset. In case of equity shares gains, holding period of 12 months is considered to determine the status i.e. STCG or LTCG.

- If holding period of a capital asset is 12 months or less, then it will be treated as a Short term capital asset and the tax rate levied will on STCG will be 15% + STT paid (if any)

- If holding period of a capital asset is 12 months or more, then it will be treated as a Long term capital asset and the tax rate levied on LTCG will be 10% without indexation. However Gains upto Rs.1 Lakh are exempted from Tax.

Suppose if 100 shares of PayTM are applied at 115Rs.each and they got listed at Rs.350 each share. Now let us say that we sell these shares after allotment, the gain would be Rs.23,500. This is the amount of capital gain.

The tax rate applicable would be 15% on Rs.23,500 which will be Rs.3,525(excluding cess+surcharge if any).

The benefit of the basic exemption limit will be applicable in case the taxpayer has only STCG income.

Set-off and carry forward of losses:

The setting off and carry forward of losses provisions of equity shares will apply to listing shares as well. In case of Short term capital loss, it will be set off against STCG or LTCG. A long term capital loss would be set off against long term capital gains only.

Any losses remaining after set off will be carried forward for 8 subsequent years.

How to report IPO gains in ITR Filing?

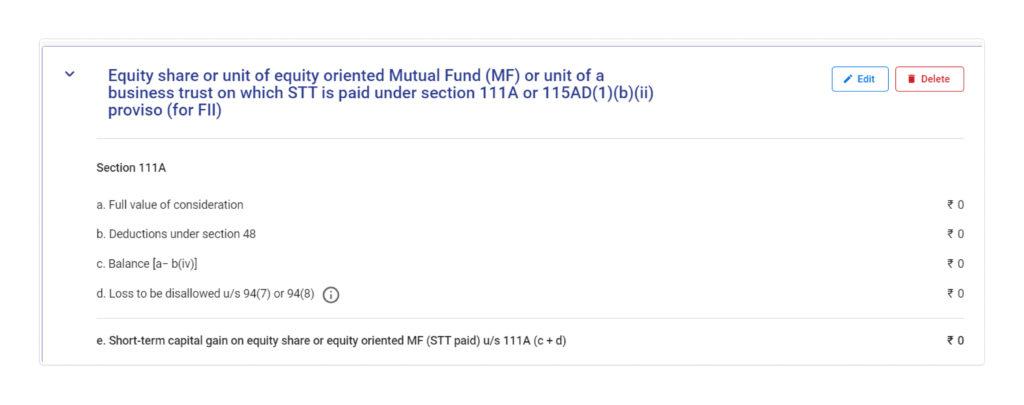

Reporting of IPO gains is to be done in either ITR-2 or ITR-3. Schedule CG should be filed for reporting details of IPO listing gains. Following details are reported in Schedule CG:

- FVOC (Full value of consideration)

- Deductions under section 48 : i) Cost of Acquisition/application ii)Transfer expenses

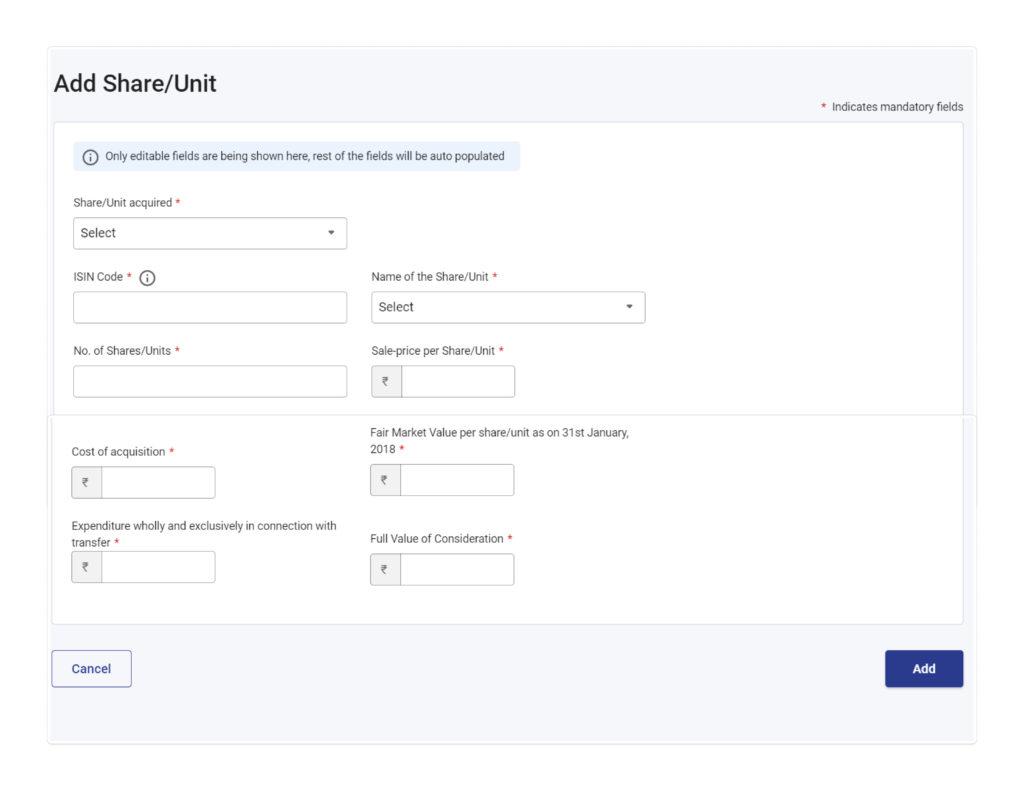

If there are any Long term capital gains as per Section 112A, then following details are to be reported:

- International Securities Identification Number (ISIN)

- Name of the share

- Number of shares sold

- Sales price per share

- Cost of acquisition

- Fair Market Value (FMV) as of January 31, 2018

- Expenditure related to the transfer

Conclusion:

Taxation of capital gains for shares listed under IPO is somewhat similar to that of taxation of capital gains for equity or equity-oriented funds. Tax rates and treatment to determine holding period is also identical. The application price is considered as cost of acquisition in such cases.

About Author:

CA Chinmay Shirish Agate

Chinmay Agate is a Practicing Chartered Accountant having 4+ years of experience and expertise in the field of Direct Taxation and Auditing compliances. In the past, he worked in various CA firms and comes with wide industry experience from services, retail to manufacturing to trading where he has handled various complex assignments. He has keen interest in Forex and Derivative knowledge as well as fundamental analysis.

Recent Comments