A partnership firm is a separate legal entity in the eyes of income tax act. It is to be assessed as a separate person apart from its partners. A partnership firm must file its Income Tax return reflecting all its business details like turnover, expenditures or profits etc. Partners of such firm are also required to file their separate individual return where the income from such partnership firm is reflected.

Partnership firms are of two types i.e. Registered Partnership firm and unregistered partnership firm.

However, it is immaterial whether a firm is registered or not, it is mandatory for firms to file income tax returns.

The expenses made by partnership firms like interest on loan or capital, salaries, commission, bonuses etc require approval in the partnership deed.

Partnership firm under Income Tax Act:

According to Income Tax Act, 1961, a partnership firm has to pay taxes as per following points:

- Income Tax @30% on Taxable Income

- Surcharge @12% if such taxable income exceeds Rs.1 cr.

- The interest on capital up to 12% is allowed as a deduction

- Health and Education cess @ 4% of the tax + Surcharge

A partnership firm is also required to pay an alternate minimum tax of 18.5% of the adjusted total income.

Deductions allowed to Partnership firm:

There are certain deductions allowed to a partnership firm for reducing its tax liability and they are as follows:

- Remuneration or interest paid to the partners of the firm which includes salary, bonuses, commission or any other remuneration paid to non-working partner as well

- Payments made to the partners which are not in accordance with the partnership deed

- Payments made to the partners related to any transaction prior to the execution of partnership deed.

Income Tax Return and Due date applicable to Partnership firm:

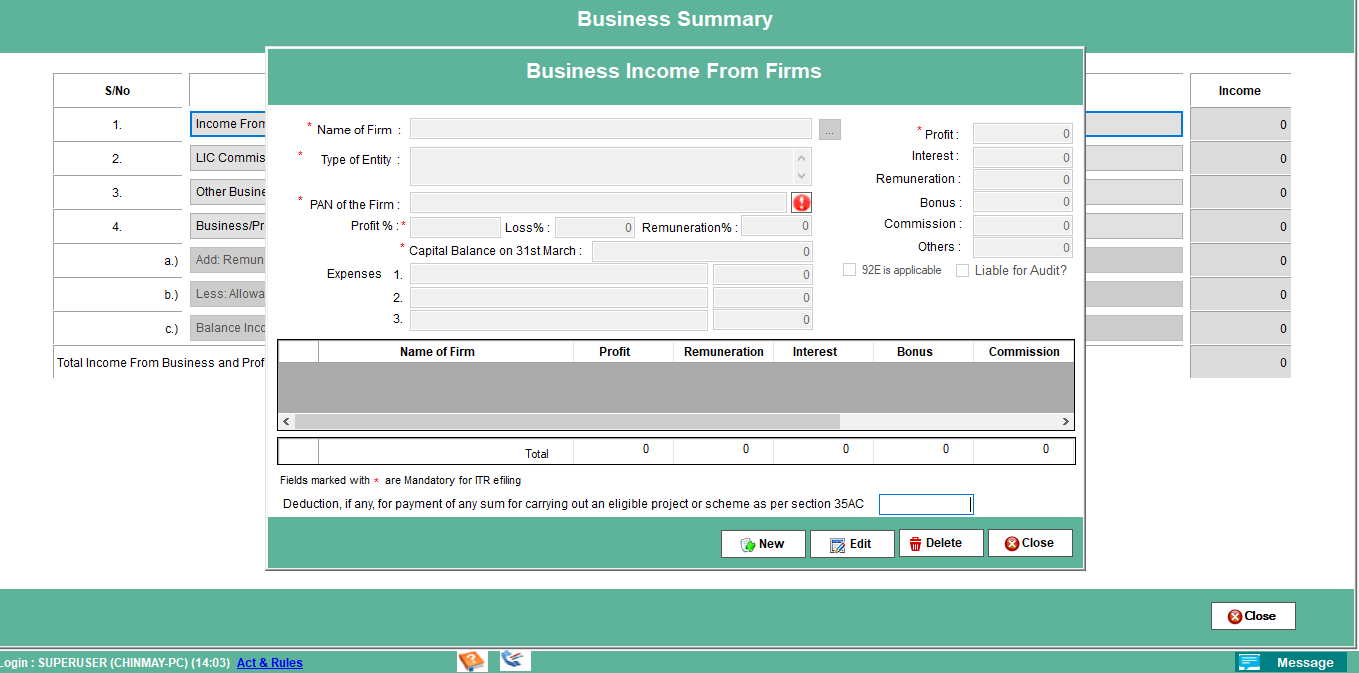

A partnership firm or LLP is required to file its income tax return in ITR-5. Firms also have an option to file their income tax in ITR-4 if they wish to declare income on presumptive basis. This form is applicable for partnership firms and not for partners of the firm. Partners have to choose either ITR-3 or ITR-4 for filing their individual income tax return. As shown in the below image, you will be able to enter required details in the taxbase software. For this you will have to first click on Income from Business/profession tab on the home scree. After that, a table will open where you have to click on the option of Income from firms and this window will open:

A partner will have to pay tax on the amount of interest, remuneration, salary, commission or bonuses etc received from the partnership firm. However, he is exempt from paying tax on the share of profit received from the partnership as the tax on the same is paid by the partnership firm itself on the entire amount of taxable profit.

The due date for filing an income tax return for a partnership firm depends upon applicability of audit to the firm. The due date for filing income tax returns are as follows:

- Firms not liable for Audit : 31st July

- Firms that are liable for Audit : 31st October

The income tax return of the partnership firm is required to be e-verified with electronic verification code. The ITR-5 can be filed without a digital signature. However, if the partnership firm is liable to audit under any section of the Income Tax Act, 1961, it must file Form ITR-5 with a digital signature certificate and e-file the audit report. The partners of the firm must also have a class 3 digital signature to verify the filing process.

Conclusion:

One must remember that while claiming deductions of interest or remuneration to partners, these must be approved by the partnership deed and are not paid in excess. The tax and surcharge rates are fixed by Income Tax Act which are irrespective of the fact that the firm is registered or not. Due date of income tax return filing depends on the applicability of audit to the partnership firm. ITR-5 is used for filing income tax returns of a firm where as ITR-3 or ITR-4 are used to file income tax returns of the partners of the firms.

About Author:

CA Chinmay Shirish Agate

Chinmay Agate is a Practicing Chartered Accountant having 4+ years of experience and expertise in the field of Direct Taxation and Auditing compliances. In the past, he worked in various CA firms and comes with wide industry experience from services, retail to manufacturing to trading where he has handled various complex assignments. He has keen interest in Forex and Derivative knowledge as well as fundamental analysis.

Recent Comments