House rent allowance (HRA) is a component of salary provided by employer to his employee, keeping in mind that employee has to bear cost of rental expenses. Salaried individuals who live in a rented house can claim this exemption and save their taxes. Taxability of HRA varies on the basis of whether you own a house and still choose to live in a rented premises or not. In this way HRA is partly taxable and partly exempt. HRA forms part of your salary itself and hence it is considered as your income only.

HRA Exemption:

The exempt amount of HRA will be calculated as follows, where exempt HRA is least of these following three:

- Actual HRA received from employer

- Rent paid – 10% of (Basic Salary+DA)

- 50% of (Basic+DA) Salary in case if employee is residing in metro cities (for non metro cities 40% of Basic+DA salary)

What are the eligibility criteria to claim exemption of HRA to employees:

Following are eligibility criteria a person needs to fulfil before claiming HRA exemption:

- Employee must be a salaried individual

- HRA is a part of salary component

- Employee is actually living in a rented premises. One may stay in a property owned by their parents and claim HRA exemption provided actual rent payments are made and parents are showing this income in their income tax return.

- Keeping in possession the documentary evidence like rent receipts or rental agreement etc.

- Self-employed individuals cannot take HRA exemption however they can claim a deduction of their rent payments under section 80GG

Documents Required for HRA Claim:

To claim HRA exemption, following documents are required:

- Rent receipts: These are proofs of payment made to landlord along with Landlord’s name PAN number and amount of rent paid etc.

- Rental Agreements: This required to consider authenticity of the claims made by employee.

- Declaration of HRA: Employers often require employees to submit a declaration form stating the amount of HRA received and the details of their rental expenses.

- Utility Bills: It is better to them handy even though they are not mandatory as it strengthens the claim of exemption made.

Let us understand the exemption HRA with an example.

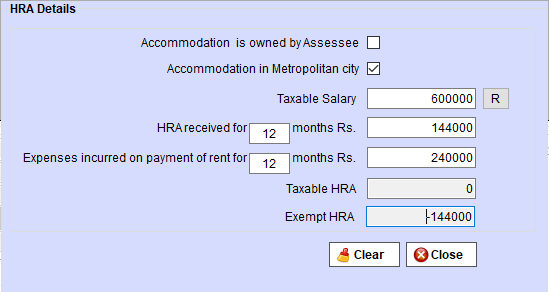

Raj is a resident of Mumbai city(metro). He earns a basic salary of Rs.50,000 per month. He earns HRA of Rs. 12,000 per month and he pays a rent of Rs. 20,000 per month.

Calculation of eligible HRA Exemption claim:

- Actual HRA Received = 12,000*12 = 1,44,000

- 50 % of Basic Salary = 50% (50,000*12) = 3,00,000

- Rent paid – 10% of Basic Salary = (20,000*12) – 10%(6,00,000) = 1,80,000

Eligible amount of HRA claim (least of the above) i.e. Rs.1,44,000.

These calculations are made easy by using Taxbase software, as you will only have to enter the amounts of Salary, HRA and rent payments. It will automatically calculate the amount of taxable and exempt HRA as shown in the given image. Untick the option of accommodation in Metropolitan city if you are ling in a non-metropolitan city.

Conclusion:

HRA is an important component of salary structure which employees often use to save their taxes. Claim of HRA depends upon multiple factors and documentation. However, this exemption is available only to those who are in employment and are not self-employed. Self-employed persons can use deduction under Section 80GG to utilise their rent payments to save taxes.

About Author:

CA Chinmay Shirish Agate

Chinmay Agate is a Practicing Chartered Accountant having 4+ years of experience and expertise in the field of Direct Taxation and Auditing compliances. In the past, he worked in various CA firms and comes with wide industry experience from services, retail to manufacturing to trading where he has handled various complex assignments. He has keen interest in Forex and Derivative knowledge as well as fundamental analysis.

Recent Comments