Taxpayers are expected to make compliance that they are required to do with the Income Tax. It may either be related to return filing of income tax or replying and adhering to notices or orders of the income tax department. However, there are instances where a taxpayer is not in agreement with the notices or orders issued by the department. In such cases he has a right to appeal against such orders with the higher authority than the one who issued such original orders.

To tackle these cases, income tax department has provided assessees with an option to file form 35 online. The list of orders against which appeals can be filed is provided under section 246A of the Income Tax Act.

What is Form 35 of the Income Tax?

Form 35 is to be filed by any assessee or a deductor aggrieved by an order of the Assessing Officer (AO). In such a case, the appeal can be filed against the order of the AO before the Joint commissioner (Appeals) or Commissioner of Income Tax (Appeals) using Form 35.

Online filing of Form 35 has been made mandatory for persons for whom e-Filing of return of income is mandatory. For persons for whom e-Filing of Return of Income is not mandatory, Form 35 can be filed either in electronic form or paper form. An appeal is required to be filed along with:

- Memorandum of Appeal ii) Statement of facts and the Grounds of appeal and

it should be accompanied by a copy of the order appealed against and the notice of demand.

Procedure to file form 35 and Appeal Schedule:

Form 35 has nine sections that you need to fill before submitting the form. These are:

- Basic Information

- Order against which Appeal is filed

- Pending Appeal

- Appeal Details

- Details of Taxes Paid

- Statement of facts, Grounds of Appeal and additional evidence

- Appeal filing details

- Attachments

- Form of Verification

Filing of form 35 is available through online mode as well as through offline mode. The procedure to file form 35 is:

- Login to Income Tax portal and select “Income Tax Forms” from E-file tab.

- Select “File Income Tax Forms” and search form 35 on the page.

- After selecting form 35, fill all the necessary fields and click on “Preview”.

- Verify details and click on “proceed to e-verify”.

- Confirm E-verification process.

- After successful verification, a success message is displayed on the screen along with the acknowledgment number and the transaction ID.

After successful verification Commissioner of Income-tax (Appeals) will schedule a hearing date and venue. Both the appellant and the Assessing Officer receive a notice specifying the date of appointment and location. Throughout the appeal proceedings, parties have the choice to participate either in person or through a representative. CIT(A) may initiate inquiries relevant to the appeal and direct the Assessing Officer to furnish a report by conducting further investigations.

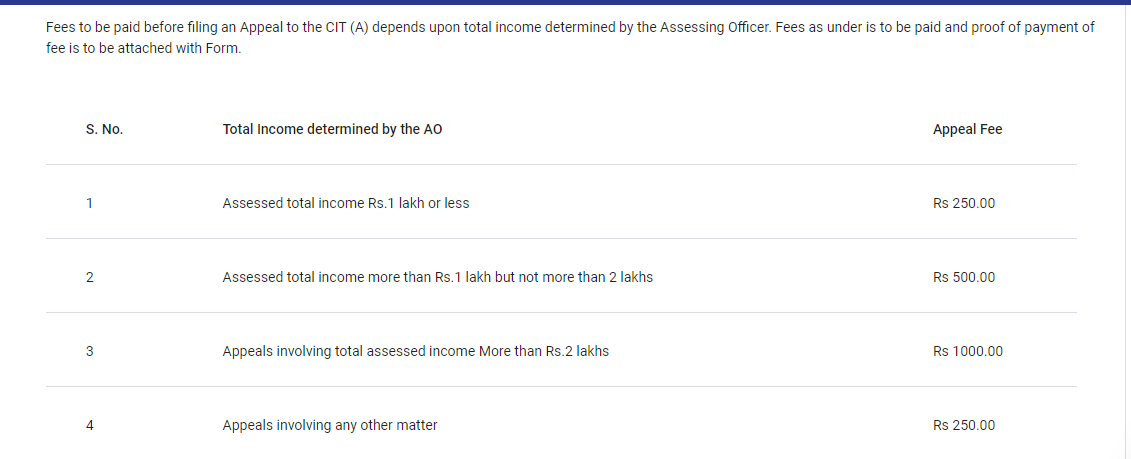

Time limit and Fees for filing an appeal:

The assessee has to file Appeal within 30 days from the date of service of order or demand as the case may be. In case you have not filed the tax return within due date then the chance to file an appeal may not be available to the assessee.

Fees for filing an appeal are:

Orders against which appeals can be made:

Section 246A of the Income Tax Act lists the appealable orders. Some of the orders against which appeal can be preferred are listed below:

- Intimation issued u/s 143(1) making adjustments to the returned income

- Scrutiny Assessment Order u/s 143(3) or an ex-parte assessment Order u/s 144, to object to income determined or loss assessed or tax determined or status under which assessed

- Re-assessment Order passed after reopening the assessment u/s 147/150

- Search Assessment Order u/s 153A or 158BC

- Rectification Order u/s 154/155

- Order u/s 163 treating the taxpayer as agent of a Non-Resident etc.

Conclusion:

Assessee has an option to file an appeal in the Form 35 either online or offline when he is aggrieved by any of the orders mentioned in section 246A of the income tax. There are many documents that are required to be submitted at the time of filing an appeal to CIT(A). The fees charged by department and time limit for filing an appeal are important aspect that an assessee has to keep in mind at the time of filing an appeal.

About Author:

CA Chinmay Shirish Agate

Chinmay Agate is a Practicing Chartered Accountant having 4+ years of experience and expertise in the field of Direct Taxation and Auditing compliances. In the past, he worked in various CA firms and comes with wide industry experience from services, retail to manufacturing to trading where he has handled various complex assignments. He has keen interest in Forex and Derivative knowledge as well as fundamental analysis.

Recent Comments