Co-operative society means a society registered under Co-operative Societies Act, 1912 or any other law in force in any State for the registration of co-operative societies. The Finance Act 2023 has introduced a new tax scheme under section 115BAE for the resident co-operative societies engaged in the manufacturing or production industry. If a co-operative society opts for this scheme, then income will be taxable at a concessional rate which is at 15% if certain conditions are fulfilled.

Section 115BAE will be applicable from 1st April, 2024 i.e. effective for AY 2024-25.

Section 115 BAE:

The concessional rate mentioned above at 15% shall be applicable to the assessees upon fulfilling certain conditions which are:

co-operative society has been set-up and registered on or after the 1st day of April, 2023, and has commenced manufacturing or production of an article or thing on or before the 31st day of March, 2024 AND i) the business is not formed by splitting up, or the reconstruction, of a business already in existence or ii) does not use any machinery or plant previously used for any purpose

- assessee is not engaged in any business other than the business of manufacture or production of any article or thing and research in relation to, or distribution of, such article or thing manufactured or produced by it. This clause does not include businesses of i) development of computer software in any form or in any media ii) mining iii) conversion of marble blocks or similar items into slabs iv) bottling of gas into cylinder v) printing of books or production of cinematograph film v) any other business as may be notified by the Central Government in this behalf

- total income of the assessee has been computed i)without any deduction under provisions of Section 10AA or Section 32(1)(iia)/33AB/33ABA or some clauses of Section 35/35AD/35CCC. ii) without set off of any loss carried forward or depreciation from any earlier assessment year, if such loss or depreciation is attributable to any of the deductions referred to in clause (i) AND iii) by claiming the depreciation, if any, under section 32, other than clause (iia) of sub-section (1) of the said section

What is Form 10-IFA:

Central Board of Direct Taxes (CBDT) has recently issued Notification No. 83/2023-Income Tax, dated September 29, 2023. This notification introduces Income Tax Rule 21AHA and Form No. 10-IFA, which are related to the exercise of an option under sub-section (5) of section 115BAE of the Income-tax Act, 1961. The introduction of CBDT Rule 21AHA and Form No. 10-IFA signifies the importance of complying with the rules and regulations governing the exercise of an option under sub-section (5) of section 115BAE of the Income-tax Act, 1961.

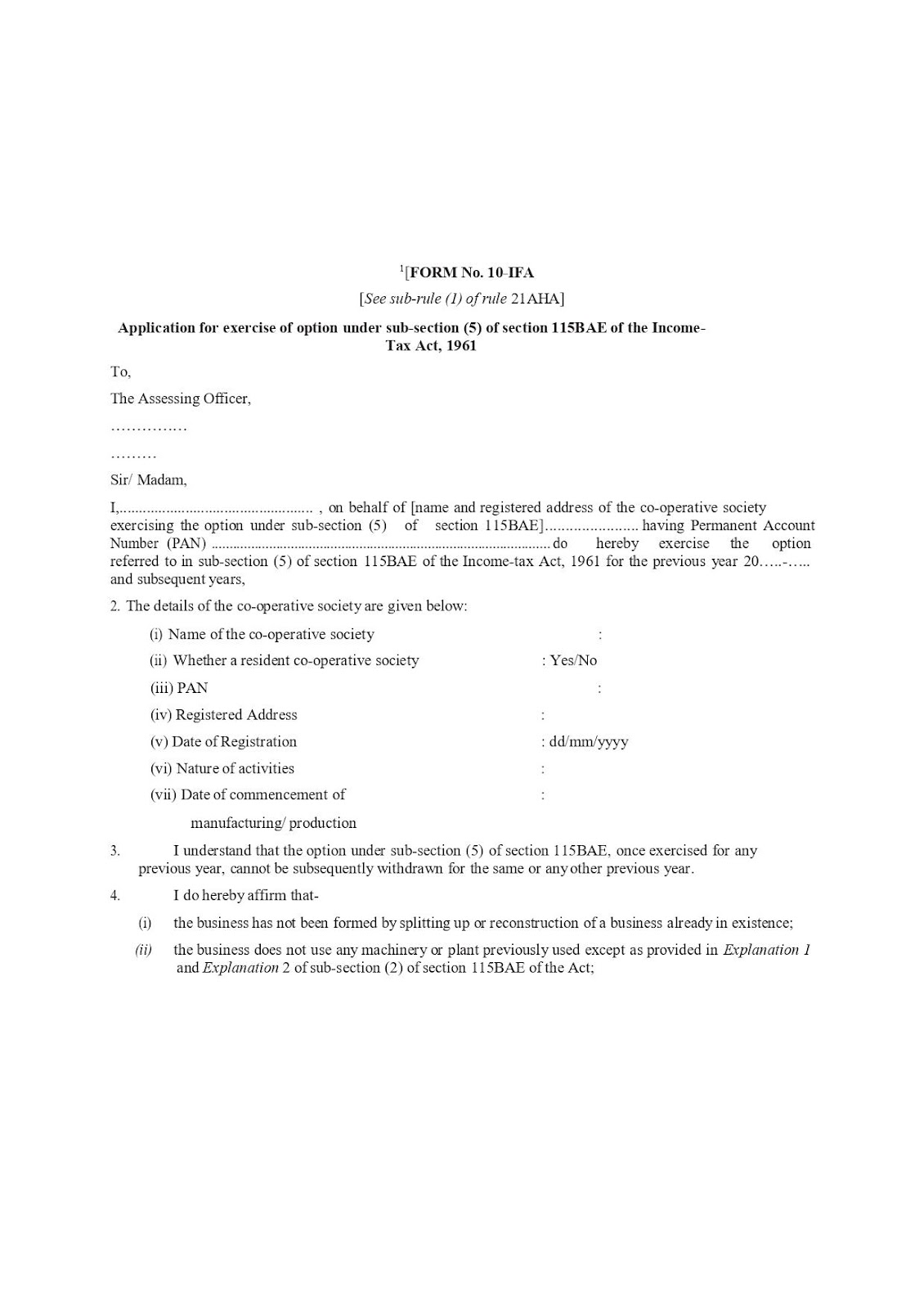

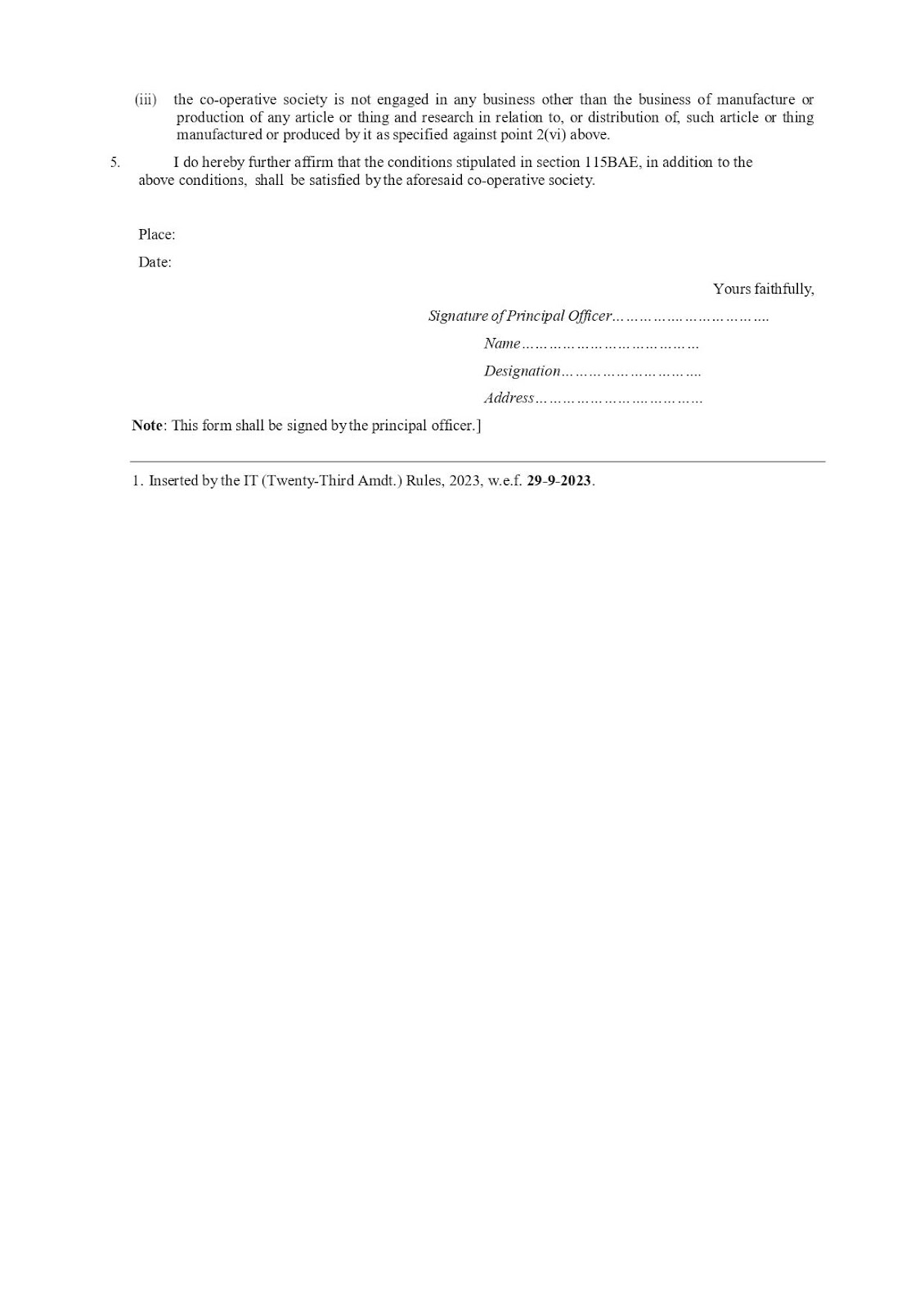

Following is the draft of Form 10-IFA:

Conclusion:

Manufacturing co-operative societies have an option to exercise under section 115BAE by filing form 10-IFA where tax rate is concessional at 15%. This form 10- IFA includes various details regarding to such co-operative societies and the details filed are to be submitted online.

About Author:

CA Chinmay Shirish Agate

Chinmay Agate is a Practicing Chartered Accountant having 4+ years of experience and expertise in the field of Direct Taxation and Auditing compliances. In the past, he worked in various CA firms and comes with wide industry experience from services, retail to manufacturing to trading where he has handled various complex assignments. He has keen interest in Forex and Derivative knowledge as well as fundamental analysis.

Recent Comments