Depreciation means reduction in the value of a particular asset due to wear and tear process. Depreciation is calculated by using two methods which are i) SLM i.e. Straight Lime Method or ii) WDV i.e. Written Down Method

Income tax allows using of WDV method for valuation of depreciable assets. Such depreciation values are allowed as an expense under income from business. There are certain instances where an additional amount of depreciation is allowed which is over and above of such normal depreciation. However, while filing written under new tax regime of Income tax, such claim of additional depreciation is not allowed.

Additional Depreciation:

When an assessee who is engaged in the business of manufacturing or production of any article or thing and he purchases new machinery or plant(excluding ships or aircrafts), and he is established after 31st March, 2005 shall be allowed additional depreciation under income tax @20% of the actual cost of the asset. When such assets is used for less than 180 days then 50%(which will be 10%) of such amount is allowed as additional depreciation. Such balance additional depreciation shall be allowed in the immediately succeeding year. This is in additional to normal rate of depreciation, For e.g if rate of depreciation on the machinery is 15% then Total rate of depreciation after additional depreciation shall be 15%+20%=35%.

Unabsorbed Depreciation Losses:

It simply means the portion of depreciation that could not be used due to non-availability of profits in the books. In such a scenario, the portion of depreciation that is unabsorbed can be carried forward to be absorbed against the future taxable profits. This amount of unabsorbed losses may also include the portion of additional depreciation that could not be absorbed.

Treatment of additional depreciation under new tax regime:

Additional depreciation under section 32 is a disallowed deduction in the new tax regime. Therefore a person filing his income tax return under new tax regime will not be allowed a deduction of additional depreciation from his income. In the case of a business income, an individual or HUF cannot claim set-off of the brought forward business loss or unabsorbed depreciation.

The assessees who had opted for income tax return filing under old tax regime till AY 2023-24 may have unabsorbed depreciation carried forward for set off which includes portion of additional depreciation also. Now under new tax regime claim of additional depreciation is not allowed.

If the assessee opts for new tax regime in AY 2024-25, he must reverse the effect of such additional depreciation carried forward from earlier years. To give effect to this situation, the amount of such additional depreciation has to be added back to the WDV of the asset in the beginning of the new financial year i.e. 01.04.2024 in this case. The amount of WDV of block of assets will increase by such amount of additional depreciation.

Let us understand this with an example.

WDV of a Machinary is Rs. 1,00,000 as on 31.03.2024.

Unabsorbed Additional Depreciation as 31.03.2024 is Rs.25,000.

Assessee opts to file Income Tax return of AY 2024-25 under new tax regime.

In the given scenario, The amount of WDV of assets in the beginning of the AY 2024-25 shall be

Opening WDV + Unabsorbed Additional Depreciations from previous assessment years

This will be Rs.1,00,000+Rs.25,000 = Rs.1,25,000.

Now the revised WDV for the calculation of depreciation in the current year shall be Rs.1,25,000.

Reporting of Changes to Opening WDV and additional Depreciation:

The addition of additional depreciation to the WDV of the asset will result in reduction of unabsorbed losses. Therefore, such amount of additional depreciation is required to be deducted from the total of unabsorbed depreciation losses carried forward.

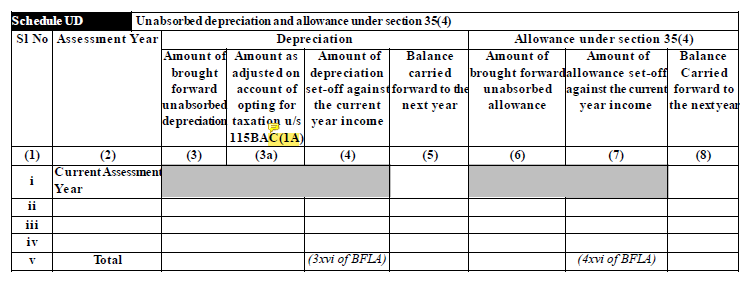

While filing Income Tax return, one has to mention these changes in the Schedule UD of ITR form.

As shown in the above image, reporting of additional depreciation is to be done for giving effect to the unabsorbed depreciation losses.

Conclusion:

New tax regime of income tax has disallowed the claim of additional depreciation in the income tax return. Therefore, it is important to make certain changes to the WDVs of block of asset for giving the effect of unabsorbed depreciations. This effect impacts the WDV of assets and balances of unabsorbed depreciations. These changes are done to streamline the process of transition from old tax regime to the new tax regime.

About Author:

CA Chinmay Shirish Agate

Chinmay Agate is a Practicing Chartered Accountant having 4+ years of experience and expertise in the field of Direct Taxation and Auditing compliances. In the past, he worked in various CA firms and comes with wide industry experience from services, retail to manufacturing to trading where he has handled various complex assignments. He has keen interest in Forex and Derivative knowledge as well as fundamental analysis.

Recent Comments