Form 10AB is an application form used in India for re-validation or renewal of existing tax exemptions or registrations under the Income Tax Act, 1961. This form is specifically for charitable or religious trusts, societies, or non-profit organizations seeking to renew their registration under section 12A/12AA or section 10(23C) of the Income Tax Act. There are generally two types of trusts: private and public trusts—which include religious and charitable trusts. Then there are statutory trusts formed by the government and quasi-government bodies which are managed by the private institutions. Certain NGOs are registered as Section 8 Companies to promote trade, art, science, charity, religion, environment protection, social welfare, sports, and research etc.

What is Form 10AB:

Since 10 AB applies to charitable trusts. NPOs/ NGOs, trusts, funds, hospitals, universities, and educational institutions get tax exemption under sections 10(23C), 12A, 12AA, 35, and 80G subject to certain conditions.

Before the Finance Act, 2020 came into action, a trust, institution, or NPO/ NGO held lifetime validity once registered unless the Income Tax Department cancelled it. However, after the introduction of this act, the registration system changed a lot. It was made completely electronic and each applicant now gets a unique registration number (URN).

Trusts, institutions, and NPOs/ NGOs earlier having a tax exemption under Sections 10 (23C), 12A, 12AA, 35, or 80G must reapply for the same and get a new registration under Section 12AB. Additionally, Section 12AB provides for tax exemption, grants from government or foreign agencies, and Foreign Contribution (Regulation) Act (FCRA) applications to get international funding.

The Finance Act, 2020 introduced the concept of permanent and provisional registrations. Two separate forms have been prescribed for a trust, institution, or NGO as per the new rules:

- Form 10A for provisional registration

- Form 10AB for conversion from provisional registration to permanent registration.

In the following instances form 10AB needs to be filed:

- Initial Registration:

This is applicable to newly established trusts and institutions aiming to claim tax benefits under sections 10(23C), 12A, or 80G of the Income Tax Act.

- Renewal of existing registration or approval:

Existing registered trusts and institutions need to renew their registration or approval every five years through Form 10AB.

- Conversion of Provisional registration to regular registration:

Form 10AB is required to be submitted if previously provisional registration is applied and received under new scheme and at least six months are not over before expiry of such provisional registration or commencement of activities.

- Modification of objectives lead to re-registration:

Re-registration is required if original objectives are not followed by trust.

- Inoperative registration needs to be activated:

If your registration under sections 10(23C) or 10(46) becomes inactive, you can activate it through Form 10AB.

How to file Form 10AB:

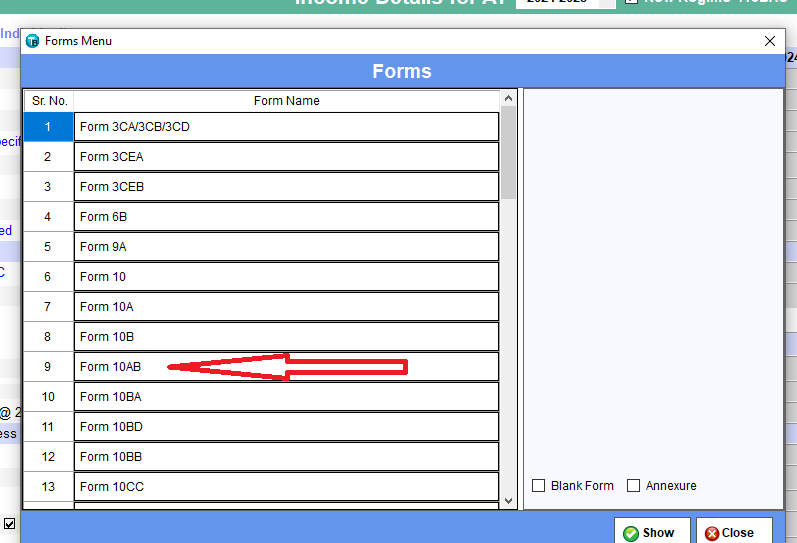

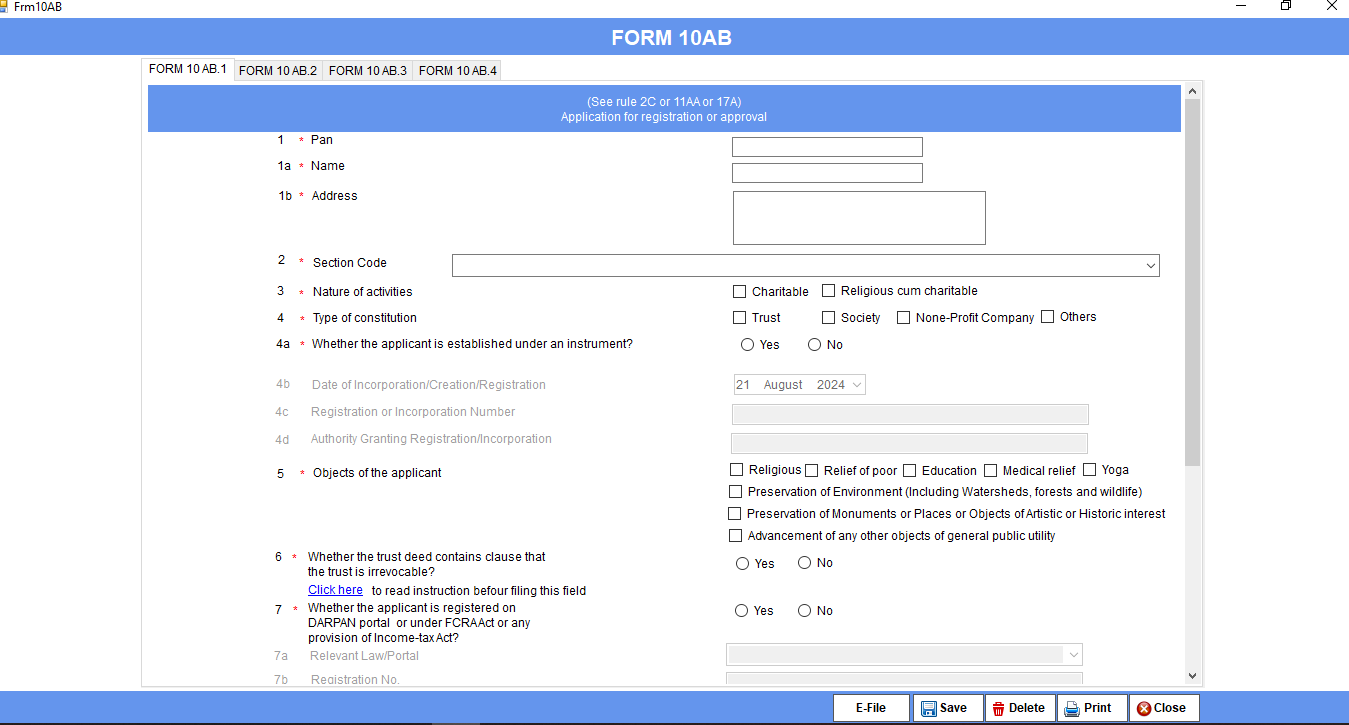

TaxBase provides the option to file the form online using the software. Once you enter the data in the software, it will automatically redirect you to the form filing portal till the verification stage. As shown in the below images you have to correctly select the form from the income screen>forms>Form 10AB option. Once form 10AB is selected, a separate window will open to enter all the required information. After entering all the required information, once you submit the form it will redirect to the e-filing portal.

Conclusion:

Form 10AB is applicable to trusts and charitable institutions rather than general businesses operating for profits. It is a form that trusts and charitable organisations need to fill to claim tax benefits under Section 10(23C), 12A, or 80G of the Income Tax Act. The form requires details regarding the activities and financials of an organisation or trust.

Chinmay Agate is a Practicing Chartered Accountant having 4+ years of experience and expertise in the field of Direct Taxation and Auditing compliances. In the past, he worked in various CA firms and comes with wide industry experience from services, retail to manufacturing to trading where he has handled various complex assignments. He has keen interest in Forex and Derivative knowledge as well as fundamental analysis.

choose from our Best Software for your business {“title”:”Read Our Latest Blogs”,”number”:”6″}

Recent Comments