A royalty refers to a payment made by one party (the licensee or user) to another (the licensor or owner) for the use of certain rights, typically related to intellectual property. These rights could include patents, copyrights, trademarks, franchises, or the rights to extract natural resources, among others.

To understand this in simple terms let us say an author of a book has approached publishers to publish the book. Publishers make profits by selling such books. An agreement is entered between publishers and authors, that an agreed sum of money will be paid to author based upon the sales or profits. This compensation is royalty.

Royalty Payments:

Royalty Payments include following amounts as incomes in it:

- Income for author’s profession

- lump sum amount for any project of writing that has a copyright of a book which may be artistic, literary or scientific in nature.

- Copyright fees received for the author’s book.

- Non-refundable advance payments of copyright fees or royalty.

Deduction under Section 80QQB:

Income from royalty payments is chargeable under the head “Profits and Gains from Business or Profession” or “Income from other sources” and income tax act also provides deduction on the same under section 80QQB.

Amount of deduction available under section 80QQB is :

Lower of

- Rs. 3,00,000 OR

- Actual amount of royalty income received

The royalties from journals, diaries, guides, newspapers, pamphlets and textbooks or any of the publications of similar nature are not eligible for deductions under section 80QQB of income tax act. Foreign income brought in India within time is eligible as deductions under section 80QQB.

Conditions to avail deductions under section 80QQB:

Eligibility to claim deductions under section 80QQB depends on the fact whether income is earned in India or not.

If income is earned in India:

- Individual must be resident or RNOR

- Author or literary, artistic or scientific work

- Filing of income tax return within time

- If an Individual has not received a lump sum amount , 15% of the value of the books sold during the year (before allowing any expenses) should be ignored.

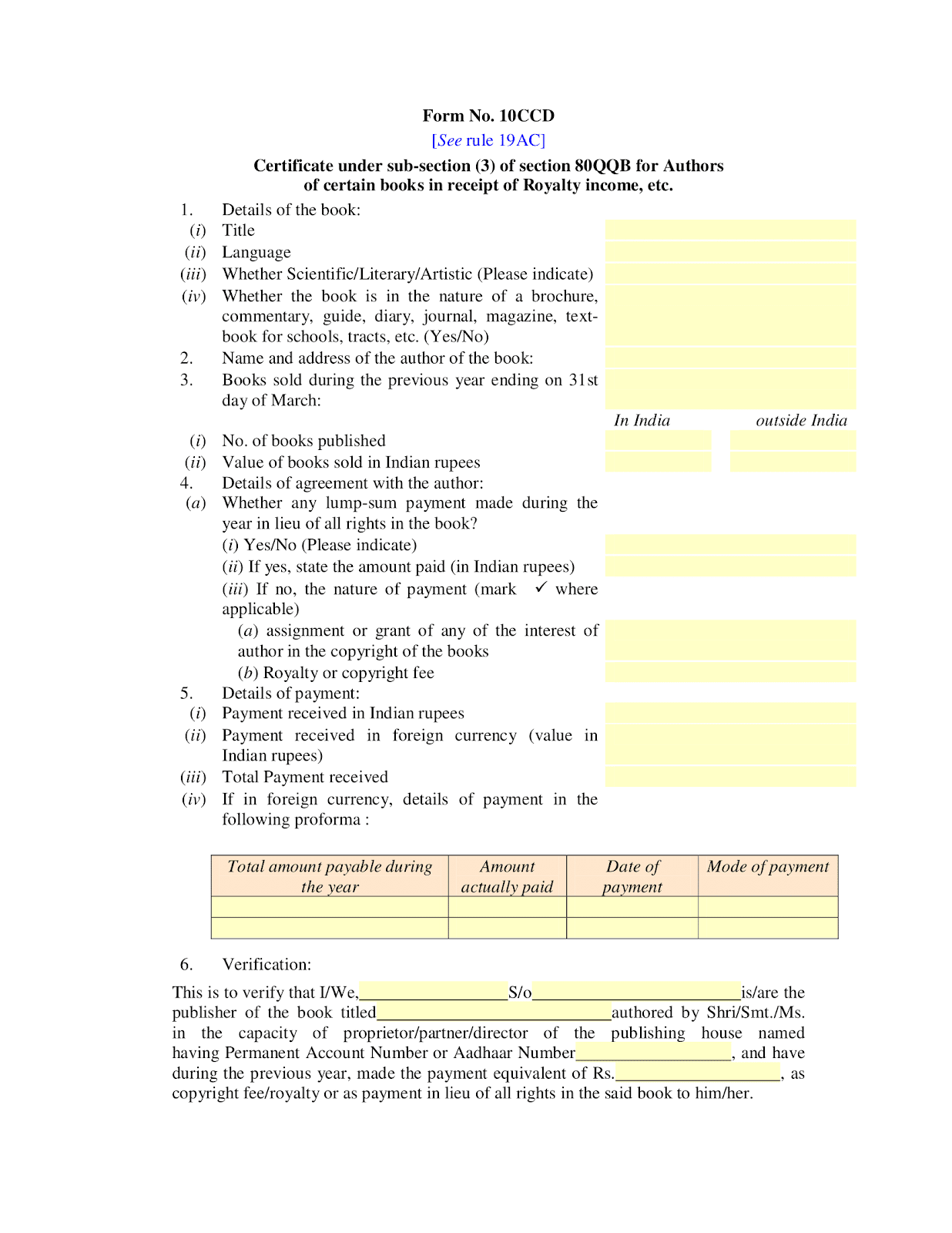

- Form 10CCD has to be obtained from the person making the payment

- To claim the deduction, return is needed to be filed under the old regime

If income is earned outside India:

- Income is brought to India in convertible foreign exchange within 6 months from the end of the year or within period as approved by the competent authority

- Certificate in Form 10H is to be obtained

Following is the Form 10CCD which should be duly filled and signed by the individual or entity making the royalty payment to the taxpayer.

Conclusion:

Authors receiving their payments in the form of royalty payments are eligible to claim a deduction from such income for a specified amount under section 80QQB. It is not available to individuals who are writing in newspapers, pamphlets, guides, textbooks , diaries, or journals. Deduction under Section 80QQB is available only to individuals.

Chinmay Agate is a Practicing Chartered Accountant having 4+ years of experience and expertise in the field of Direct Taxation and Auditing compliances. In the past, he worked in various CA firms and comes with wide industry experience from services, retail to manufacturing to trading where he has handled various complex assignments. He has keen interest in Forex and Derivative knowledge as well as fundamental analysis.

choose from our Best Software for your business {“title”:”Read Our Latest Blogs”,”number”:”6″}

Recent Comments